Text Summary via OCR:

|

among contractors, ures show: |

the credit |

agency's fig- |

|

Year |

Failures |

Year |

Failures |

|

1951........ |

____ 957 |

1954... |

.........1,305 |

|

1952........ |

____ 838 |

1955... |

.........1,404 |

|

1953........

*Jan.-Apr. |

____1,024 |

1956... |

......... 570* |

Some publications have projected these figures into percentage increases in failures. This is probably inaccurate, since the total number of contracting firms is not updated

A major fight is shaping up to save the package mortgage.

The outcome will affect every builder who sells built-in appliances and equipment under VA or FHA mortgages.

Retail furniture dealers and appliance men, anxious to regain the business they lost when builders began installing household equipment in new homes, attacked package mortgages as unsound in testimony before the Senate housing subcommittee earlier this year. They argued that home buyers were paying four times what they should for "fast-wasting asset-� when they are financed under 30-year mortgages.

Lobbyist Julian W. Caplan of the Natl. Retail Furniture Assn, testified that $500 of carpeting financed on a three-year term at 7% involved "total interest and credit service charges of $105,"� and monthly payments of $16.80. On a 30-year mortgage at 5%, inter: est would reach $618, he complained.

(He did not point out that: 1) monthly payments on the package mortgage would be only $2.68 instead of $16.80, 2) the average FHA and VA mortgage is paid off in 12 years instead of 20 or 30 [which would mean a total interest cost of only $239.32 on $500 of equipment], 3) installation charges on built-in household equipment like air condi-

yearly by the Commerce Dept. Last time Commerce counted, in 1951, it found 390,000 contractors. There are no federal figures on how many were home builders.

Most failures occur with general contractors (building constructors), D&B says. Strangely enough, one cause may be the boom itself. Reason: Some contractors take on too many jobs, spread themselves too thin. If anything goes awry, they crack and go under.

tioners, refrigerators, stoves, dishwashers, disposers bought through retailers or discount houses sometimes equal the original cost of the item thus canceling out the entire "saving,"� 4) neither FHA nor the building industry has any intention of including carpeting which does wear out rapidly on mortgages, anyway and 5) mortgage interest rates are low enough so it is often cheaper to borrow to install, say, a new kitchen even if you have the cash on hand. Reason: the same money can earn more invested than the interest will cost.)

Senators call for a study

At first, the building industry did not take the attack seriously. Retailers had made efforts before to legislate their competition out of business instead of trying to compete.

But the Senate banking committee, in a surprise move, went so far as to consider amending the National Housing Act to bar FHA mortgages on equipment which would not "continue to enhance the security and value of the property for the duration of the mortgage period."� Opposition inside the committee beat down the move, but the senators did ask FHA to report on what such a ban might mean. Specifically, FHA was told to

list 1) what items would be barred from mortgage-insurance under the proposed amendment, 2) how this might affect "size and utility"� of FHA-backed homes, 3) "advantages and disadvantages to the home owner, 4) what effect the ban would have on industries producing household equipment and 5) how the ban would affect the home building industry.

With FHA scheduled to report back to the committee by Jan. 31, appliance dealers are looking for industry support and even leadership for their fight. Their reason is obviou-�it's now estimated that $45 million a year of major appliances sold are sold through builders in new homes on a package mortgage.

Ironically, the furniture men would probably be hurt more than the appliance industry if package mortgages were killed. A new homeowner will always buy a stove and refrigerator some way. But if he has to buy this equipment with his limited amount of cash or on short term credit, he certainly would have much less to invest initially in furniture.

More built-ins

While retailers were agitating against the package mortgage and presumably with it the entire line of built-in appliance-�more manufacturers were adding built-ins to their lines. Items:

•� Servel Inc., biggest maker of gas refrigerators, announced that every refrigerator in its line will be designed to fit recessed, built-in installation.

•� Norris-Thermador announced its first built-in electric refrigerator, a self-contained stainless steel unit.

And while the fight over package mortgages grew hot, Sen. John Sparkman (D, Ala.), chairman of the Senate housing subcommittee, suggested that FHA ease up on Title I improvement loans and allow home-owners to use them to buy major appliances. FHA now restricts Title I to items which are a part of the home and are not free standing.

NEWS continued on p. 44

Fight looms on package mortgages as retailers urge Congress to ban them

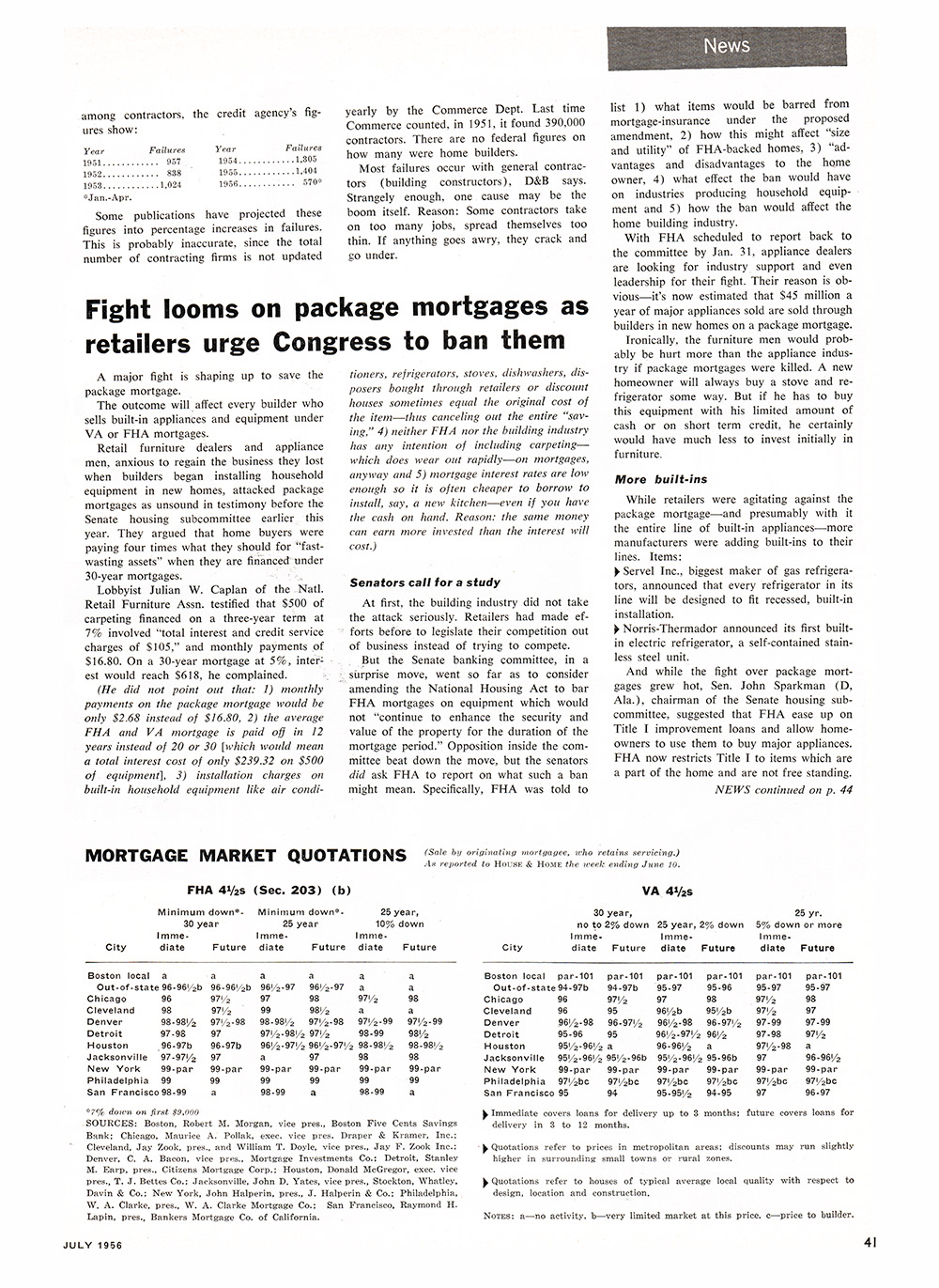

MORTGAGE MARKET QUOTATIONS (Sale by originating mortgagee, ivho retains servicing.)

As reported to House & Home the iveek ending June 10.

FHA 4V2s (Sec. 203) (b)

Minimum down*- Minimum down*- 25 year,

30 year 25 year 10% down

Imme- Imme- Imme-

City diate Future diate Future diate Future

|

Boston local |

a |

a |

a |

a |

a |

a |

|

Out-of-state 96-96/2b |

96-96/2b |

96/2-97 |

96/2-97 |

a |

a |

|

Chicago |

96 |

97/2 |

97 |

98 |

97/2 |

98 |

|

Cleveland |

98 |

97/2 |

99 |

98/2 |

a |

a |

|

Denver |

98-98/2 |

97/2-98 |

98-98/2 |

97/2-98 |

97/2-99 |

97/2-99 |

|

Detroit |

97-98 |

97 |

97/2-98/2 97/2 |

98-99 |

98/2 |

|

Houston |

96-97b |

96-97b |

96/2-97/2 |

96/2-97/2 98-98/2 |

98-98/2 |

|

Jacksonville |

97-97/2 |

97 |

a |

97 |

98 |

98 |

|

New York |

99-par |

99-par |

99-par |

99-par |

99-par |

99-par |

|

Philadelphia |

99 |

99 |

99 |

99 |

99 |

99 |

|

San Francisco 98-99 |

a |

98-99 |

a |

98-99 |

a |

*7% down on first $9,000

SOURCES: Boston, Robert M. Morgan, vice pres., Boston Five Cents Savings Bank; Chicago, Maurice A. Poliak, exec, vice pres. Draper & Kramer, Inc.; Cleveland, Jay Zook, pres., and William T. Doyle, vice pres., Jay F. Zook Inc.; Denver, C. A. Bacon, vice pres., Mortgage Investments Co.; Detroit, Stanley M. Earp, pres., Citizens Mortgage Corp.; Houston, Donald McGregor, exec, vice pres., T. J. Bettes Co.; Jacksonville, John D. Yates, vice pres., Stockton, Whatley, Davin & Co.; New York, John Halperin, pres., J. Halperin & Co.; Philadelphia, W. A. Clarke, pres., W. A. Clarke Mortgage Co.; San Francisco, Raymond H. Lapin, pres., Bankers Mortgage Co. of California.

VA 4VaS

30 year, 25 yr.

no to 2% down 25 year, 2% down 5% down or more Imme- Imme- Imme-

|

City |

diate |

Future |

diate |

Future |

diate |

Future |

|

Boston local |

par-101 |

par-101 |

par-101 |

par-101 |

par-101 |

par-101 |

|

Out-of-state 94-97b |

94-97b |

95-97 |

95-96 |

95-97 |

95-97 |

|

Chicago |

96 |

97/2 |

97 |

98 |

97/2 |

98 |

|

Cleveland |

96 |

95 |

96/2b |

95/2b |

97/2 |

97 |

|

Denver |

96/2-98 |

96-97/2 |

96/2-98 |

96-97/2 |

97-99 |

97-99 |

|

Detroit |

95-96 |

95 |

96½-97½ 96½ |

97-98 |

97/2 |

|

Houston |

95/2-96/2 a |

96-96/2 |

a |

97/2-98 |

a |

|

Jacksonville |

95/2-96/2 95/2-96b |

95/2-96/2 95-96b |

97 |

96-96/2 |

|

New York |

99-par |

99-par |

99-par |

99-par |

99-par |

99-par |

|

Philadelphia |

97/2bc |

97/2bc |

97/2bc |

97/2bc |

97/2bc |

97/2bc |

|

San Francisco 95 |

94 |

95-95/2 |

94-95 |

97 |

96-97 |

y Immediate covers loans for delivery up to 3 months; future covers loans for delivery in 3 to 12 months.

y Quotations refer to prices in metropolitan areas; discounts may run slightly higher in surrounding small towns or rural zones.

^ Quotations refer to houses of typical average local quality with respect to design, location and construction.

Notes: a no activity, b very limited market at this price, c price to builder.