Text Summary via OCR:

continued from p. 37

MORTGAGE MARKET:

Money pinch should get no worse, experts say; easing foreseen in fall

The mortgage market apparently has touched bottom. It may not ease notably until September or October (or perhaps later), but mortgage men across the nation say it should get no tighter.

Discounts on VAs and FHAs actually rose a little last month in many cities. But this was chiefly the expected adjustment of the mortgage market to the new high price of money. More builders were deciding to swallow another ½ point or 1 point in discount rather than gamble on a low standby commitment with warehousing. "Every month there's a little more giving 'way by builders,"ť says one West Coast lender. FNMA prices help bar any further price slide for FHA and VA paper, too. FNMA volume continues to increase.

Mutual savings banks are beginning to show more interest in buying.

This has not meant an upsurge in loan volume, just a portent of what is to come. Volume of secondary market commitments is still thin as it has been since the mortgage market tightened abruptly in April. Drying up of the usual flow of out-of-state money from New York and New England mutual savings banks has hurt housing in areas like Florida, Texas and California which depend heavily on outside money to finance new homes for their growing populations. Now the outlook is changing. Says Pres. Stanley Earp of Detroit's Citizen's Mortgage Corp.: "Many lenders are showing more interest now that they realize the market has hit bottom and will go only up from here. They're willing to make commitments while they can still get paper at today's low prices."ť

Opinions differ on how soon the mortgage market will ease enough to make discounts on 4½% government-backed mortgages shrink again.

Some mortgage bankers look for first signs of easing this month, perhaps when life insurance companies set quotas for the second half of the year. Most experts think the easing will come no sooner than September, or October. But President Walter H. Dreier of the US S & L League says: "Any one planning to build a house in 1956 should do so in expectation that mortgage terms during the remainder of the year will remain essentially the same as they are now."ť

On the other hand, falling starts may mean many outstanding commitments will not be filled. Mortgages seeking lenders will be scarcer by fall.

Savings deposits are rising again good news for builders if the trend continues. The drop in savings had worried administration officials. Americans saved about $17 billions in 1955. That was less than in 1954, and 1954 savings were a little lower than 1953. It means the US is not saving enough money to finance the rapid growth of which its economy is otherwise capable.

Construction money grew even harder to get last month. Some of this was the expected June pinch on credit in general. Some of it, lenders say, is fear of unsold homes. But this should be a very temporary squeeze.

The Federal Reserve's step-up of open market buying of short-term government obligations eased short-term money (e. g. construction loans) a little, although the effect was not felt in the mortgage market.

But prices of Treasury bonds are rising again. Mortgages always lag behind when interest rates and bond yields change. One White House aide predicts the Fed's latest moves will keep starts up to the 1.1 million mark this year, and perhaps help boost them slightly higher.

The Fed hit back at critics in and out of Congress who say its policy of tightening money to avert inflation is hurting construction disproportionately. The money managers called the rise in mortgage debt during the first four months of this year "large"ť compared to any year but 1950 when housing set its all time record. The Fed still expects new housing, dollarwise, to equal last year's $16 billion, despite fewer starts.

On balance, slow sale-”not tight mortgage money have been the big brake on new housing so far this year, despite cries of NAHB officials to the contrary. This is particularly true in big metropolitan areas that have seen the biggest booms on easy-money terms during the last 12 months.

MORTGAGE BRIEFS

Discounts climb ½ point

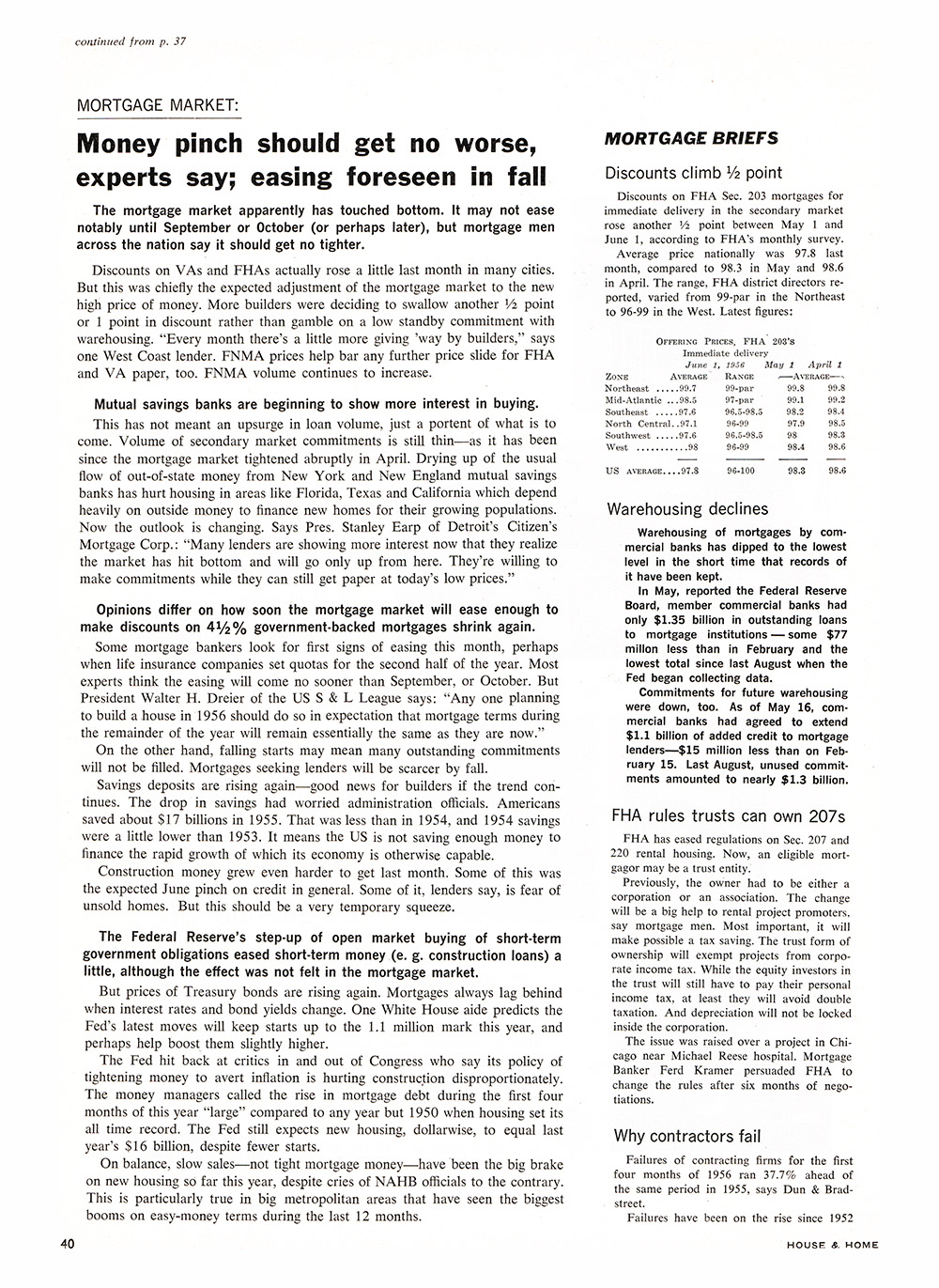

Discounts on FHA Sec. 203 mortgages for immediate delivery in the secondary market rose another ½ point between May 1 and June 1, according to FHA's monthly survey.

Average price nationally was 97.8 last month, compared to 98.3 in May and 98.6 in April. The range, FHA district directors reported, varied from 99-par in the Northeast to 96-99 in the West. Latest figures:

Offering Prices, FHA 203's

Immediate delivery June 1, 1956 May 1 April 1 Zone Average Range , Average

Northeast .....99.7 99-par 99.8 99.8

Mid-Atlantic ...98.5 97-par 99.1 99.2

Southeast .....97.6 96.5-98.5 98.2 98.4

North Central. .97.1 96-99 97.9 98.5

Southwest.....97.6 96.5-98.5 98 98.3

West ...........98 96-99 98.4 98.6

US average____97.8 96-100 98.3 98.6

Warehousing declines

Warehousing of mortgages by commercial banks has dipped to the lowest level in the short time that records of it have been kept.

In May, reported the Federal Reserve Board, member commercial banks had only $1.35 billion in outstanding loans to mortgage institutions some $77 millon less than in February and the lowest total since last August when the Fed began collecting data.

Commitments for future warehousing were down, too. As of May 16, commercial banks had agreed to extend $1.1 billion of added credit to mortgage lender-”$15 million less than on February 15. Last August, unused commitments amounted to nearly $1.3 billion.

FHA rules trusts can own 207s

FHA has eased regulations on Sec. 207 and 220 rental housing. Now, an eligible mortgagor may be a trust entity.

Previously, the owner had to be either a corporation or an association. The change will be a big help to rental project promoters, say mortgage men. Most important, it will make possible a tax saving. The trust form of ownership will exempt projects from corporate income tax. While the equity investors in the trust will still have to pay their personal income tax, at least they will avoid double taxation. And depreciation will not be locked inside the corporation.

The issue was raised over a project in Chicago near Michael Reese hospital. Mortgage Banker Ferd Kramer persuaded FHA to change the rules after six months of negotiations.

Why contractors fail

Failures of contracting firms for the first four months of 1956 ran 37.7% ahead of the same period in 1955, says Dun & Brad-street.

Failures have been on the rise since 1952